From a five-minute video you can see at Lars P. Syll... naked capitalism... heteconomist... EconoMonitor...

Syll says "Just watch it", but I can't. I have to say something. When I see something wrong, I have to say something. Don't you?

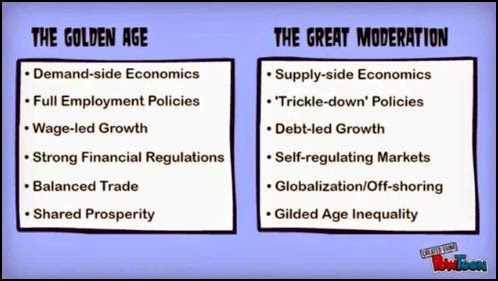

Here's a snapshot from the video:

Third item on the lists says there was a change from "wage-led growth" to "debt-led growth". I have trouble with that. It suggests new borrowing grew significantly faster in the later period. But that's not correct.

Back in March, at New Left Project, Andrew Kliman evaluated Sam Gindin's take on the global economic crisis. Kliman wrote:

According to Gindin, workers’ incomes stagnated as their wages declined or grew slowly. This not only boosted profits but also contributed substantially to the growth of the financial sector as workers became 'dependent on credit' in order to keep their standard of living from falling. In particular, they 'came to depend heavily on their homes as collateral for borrowings.'

However, although Gindin cites a lot of data elsewhere in his article, almost no hard evidence accompanies this account of capitalism under 'neoliberalism,' and the hard evidence fails to support much of it. Since something like this account has become conventional wisdom among much of the Left, it is important to review the facts in detail.

According to Kliman, the "conventional wisdom" is not correct. He says

the share of personal consumption spending funded by consumer credit––i.e. all household borrowing except for home mortgages––did not rise over time. In other words, consumption did not increasingly come to depend on consumer credit.

Consumption did not increasingly come to depend on consumer credit.

That assertion of Kliman's stopped me cold the first time I read his article. It should make you stop, too. It should make you second guess yourself, as it did me.

Well, maybe you don't like second guessing yourself. But I'm pretty sure you do like this: the Fisher Dynamics of household debt. As Mark Thoma said,

this research knocks a hole in the story that it was lack of self control ... that caused the increase in household debt prior to the financial crisis

When Thoma says it wasn't a lack of self-control, he means it wasn't increased borrowing that caused debt to increase. At Thoma's link, JW Mason summarizes the research:

It’s a well-known fact that household debt has exploded in recent decades, rising from 50 percent of GDP in 1980 to over 100 percent on the eve of the Great Recession. It’s also well-known that household borrowing has increased sharply over this period. ... In fact, though,... while the first [of these] is certainly true, the second is not.

Mason says the same thing as Kliman: We think consumption increasingly came to depend on credit since 1980, but that's not correct.

Now you have to stop and think.

Now you have to take a step back from the conventional wisdom. Doesn't matter how cute that five-minute video was.

We have to get this right.

Debt grew faster after 1980 than before, not because of an increase in borrowing, but because of the disinflation.

7 comments:

But look at household debt/consumption expenditures.

http://research.stlouisfed.org/fred2/graph/?g=Aqm

Doesn't this contradict Kliman?

Cheers!

JzB

the share of personal consumption spending funded by consumer credit––i.e. all household borrowing except for home mortgages––did not rise over time. In other words, consumption did not increasingly come to depend on consumer credit.

Consumption did not increasingly come to depend on consumer credit.

I wonder about setting the scope to exclude home mortgages, especially using Thoma's comment as a follow up:

this research knocks a hole in the story that it was lack of self control ... that caused the increase in household debt prior to the financial crisis

What gets lost there is the house-as-ATM contribution to consumer spending prior to the crisis. The housing bubble wasn't just a nebulous wealth effect, people were piling on debt by borrowing against home equity and spending the money. There were even vehicles that gave you a card or a checkbook that let you spend your home equity like it was a checking account balance.

There was a direct, debt-fueled conduit from home price increases to consumer spending.

First of all, it would be Borrowing-led Growth, not Debt-led. Borrowing creates the money that boosts the spending that we think of as aggregate demand. When the money's gone nothing remains but the debt, and debt is anything but a boost to the economy.

Kliman separates "consumer credit" from mortgage debt and says consumer credit is not going up. Yeah, maybe that is a weak argument...

Mason admits that consumer borrowing increased since the 2000s (I think) but not before. And debt was increasing, before. And Mason's argument is strong I think.

My part in this comes at the end of the post: Debt grew faster after 1980 because of the disinflation. I think Mason would see disinflation as one of a few parts of the Fisher Dynamics that drove debt up... It's the one I can see and measure.

I think the bubble in housing prices came late in the Great Moderation; but debt was going up all the while. The housing bubble explains only the tail end of it.

First of all, it would be Borrowing-led Growth, not Debt-led. Borrowing creates the money that boosts the spending that we think of as aggregate demand. When the money's gone nothing remains but the debt, and debt is anything but a boost to the economy.

The point about creating money that boosts spending is well taken, it's exactly what I was getting at.

However, I don't understand at all what the distinction between borrowing and debt you're making is or how taking on debt by borrowing against home equity to fund spending is categorically different from taking on debt by using a credit card to fund spending where the former has to be called "borrowing led" and the latter "debt led".

I think the bubble in housing prices came late in the Great Moderation; but debt was going up all the while. The housing bubble explains only the tail end of it.

I agree with that but the dynamics at the tail end are of some interest in their own right as that's where it blew up. Specifically as a response to Thoma's comment about the run-up to the crisis.

Number one, Kliman's article was full of things I strongly disagreed with and things I strongly agreed with. Two months later, and those conflicts are still festering. Bringing the topic up, I don't mean to take Kliman's side but rather to get help in thinking about it. So, thank you geerussell, Jazzbumpa, for the help.

Kliman's view does seem rather silly now. His claim "all household borrowing except for home mortgages––did not rise over time" doesn't lead to his conclusion that "consumption did not increasingly come to depend on consumer credit." It is like saying spending out of the left-hand pocket did not increase and yeah, spending out of the right-hand pocket *did* increase, but we can look at the left-hand pocket spending and conclude that spending didn't increase.

I'll have to go read the Kliman piece again to see if this objection to it is valid, but from here it seems right. His argument seems weak to me now.

//

Geeerussell: "I don't understand at all what the distinction between borrowing and debt you're making is..."

Borrowing is a boost and repayment of debt is a drag on economic performance. Nobody sees this distinction for some reason. "Hey, where'd this big pile of dirt come from?" ... "It came out of that hole there." Only with borrowing, you don't get a big pile of dirt. With borrowing, each shovel of dirt gets spread out over the whole garden. Gradually, the surface level of the garden soil rises. (That's inflation.) Then one day you trip and fall into the hole. That's the crisis.

Hey, the boost to the economy has to come from somewhere. If we say we're spending future money, then the boost comes from the future. When we get to the future we have to borrow even more, or the drag created by repayment is a problem. For a while, borrowing more is natural. After a while, not so much. And eventually, just knowing that there will be a problem becomes a problem. But at that point the system is fragile, and a little hesitation in borrowing is enough to bring down the whole house of cards.

If increased spending (i.e. increased quantity of money) leads to inflation, the increased prices make the extra money necessary, so that the money isn't "extra" any more. Of course, there is still the interest cost and the repayment to deal with. When the crisis comes, one scenario is for prices to go back down, so that the money is "extra" again, so we can use it to pay off debt. But apparently, sticky prices disallow that scenario.

I argue for accelerated repayment of debt, so that the money gets repaid while it is still "extra" as a way to fight inflation, and to prevent debt accumulation from reaching problematic levels. But I'm off-topic again.

"...or how taking on debt by borrowing against home equity to fund spending is categorically different from taking on debt by using a credit card to fund spending..."

I now agree, it is not categorically different.

"...where the former has to be called "borrowing led" and the latter 'debt led'."

Sorry, I didn't mean to say that. It was sort of a tangent when I said "First of all, it would be Borrowing-led Growth, not Debt-led." That's my standard complaint that applies everywhere. I should have omitted it here and stayed on topic.

//

From the Abstract of Mason and Jayadev's Fisher Dynamics in Household Debt:

"Specifically, if average rates of growth, inflation and interest remained the same after 1980 as before 1980, household debt burdens in 2011 would have been roughly the same as they were in the early 1950s, despite the sharp increase in borrowing in the early 2000s."

I have to feed the dogs. I have to stop proof-reading now. Dammit!

My point was that consumer credit didn't rise in relation to consumption spending, AND that home mortgage borrowing also didn't rise in relation to consumption spending, prior to the late 1990s. So spending fueled by a relative increase in household debt was not a feature of "neoliberalism" *in general*. ... In a follow-up piece on NLP, I also show that consumption spending didn't rise as a share of income--when we define income as after-tax income + changes in net worth disposable income--except briefly at the start of the last decade when net worth plummeted after the bursting of the dot-come bubble.

After a long delay I am back at this post.

In a comment above, Mr. Kliman writes: "My point was that consumer credit didn't rise in relation to consumption spending, AND that home mortgage borrowing also didn't rise in relation to consumption spending, prior to the late 1990s."

See that "AND" there? I shortened an excerpt I took from Kliman's article for the post. My bad. Here's a more complete excerpt:

"It shows, first, that the share of personal consumption spending funded by consumer credit––i.e. all household borrowing except for home mortgages––did not rise over time. In other words, consumption did not increasingly come to depend on consumer credit. Second, while there was a huge rise in mortgage borrowing as a percentage of consumption spending, that rise was limited to the period of the housing bubble, which began in the late 1990s.[2] It was not characteristic of the 'neoliberal period' as such."

My apologies to you, Mr. Kliman. Thank you for the visit and for the correction.

Post a Comment