JW Mason writes:

Changes in debt-income ratios reflect a number of macroeconomic variables, and until you have a specific story about which of those variables is driving the debt-income ratio, you can't say what relationship to expect between that ratio and demand.

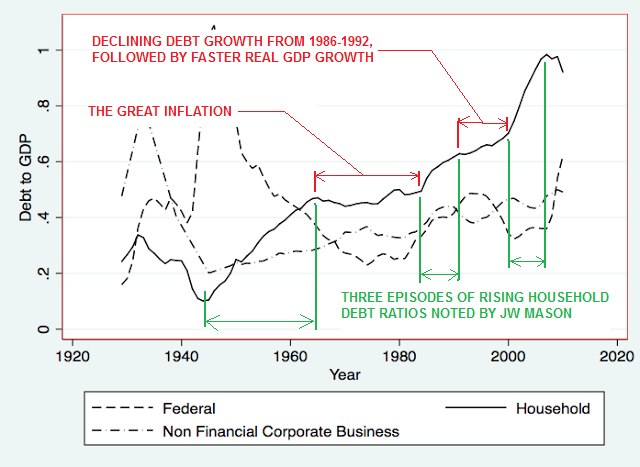

Figure 1 shows the trajectory of household debt for the US since 1929, along with federal debt and non financial business debt. (All are given as fractions of GDP.) As we can see, there have been three distinct episodes of rising household debt ratios since World War II: one in the decade or so immediately following the war, one in the mid-1980s, and one in the first half of the 2000s.

Here, let me mark up his graph:

Wow, that was tedious. I have to find a better way to mark up graphs than Paint.

Anyway, in green I show (roughly) the "three distinct episodes of rising household debt" noted by Mason in the excerpt. In red I show the two intermissions between those episodes, and label the intermissions with "specific stories" about which variables are driving the debt/income ratio.

I considered the intermission labeled "The Great Inflation" in my Debt is a red herring post, and I suppose in all of my stuff on the erosion of debt by inflation.

I considered the second intermission several times also... The slowdown in debt growth that began in the mid-1980s in A second look at the heteconomist post... The increase in the rate of money growth in The Money Growth Component... The superior growth of real GDP in the latter 1990s in Assimilate This...

Mason is right: There are many variables because of which the debt/income ratio may change. But more than that: There are secrets hidden within those variables, secrets that can open the door to improved economic growth on a more-or-less permanent basis.

If only we pick the right door.

No comments:

Post a Comment